Key Challenges Women Face that Impact Their Financial Security

As we celebrate Women’s History Month, it’s an opportunity to highlight both the challenges and growing opportunities shaping women’s experiences as they age. For women ages 50 to 64, this pivotal stage is influenced by caregiving, work, and rising healthcare needs -- alongside emerging efforts to better support well-being and stability over time.

March 27, 2026Planning for retirement is difficult at any age, but it can be especially challenging for women ages 50 to 64, who are often juggling work, caregiving responsibilities, and rising health expenses associated with an increase in health care needs. These years are also often women’s peak earning years, making this period a critical window to build savings and strengthen financial security. Elder Index data show that half of older adults over age 65 living alone and 20% of older couples cannot afford the basic needs, like housing, food, and health care, without assistance. However, this burden falls especially hard on women, who are more likely than men to live in poverty. These data points show why tackling these challenges early is essential for long-term financial stability.

How Women are Affected Over Time

Economic security challenges for women often begin before retirement and compound over time, making it critically important to address the women’s financial needs earlier. Several key factors impact financial stability for women.

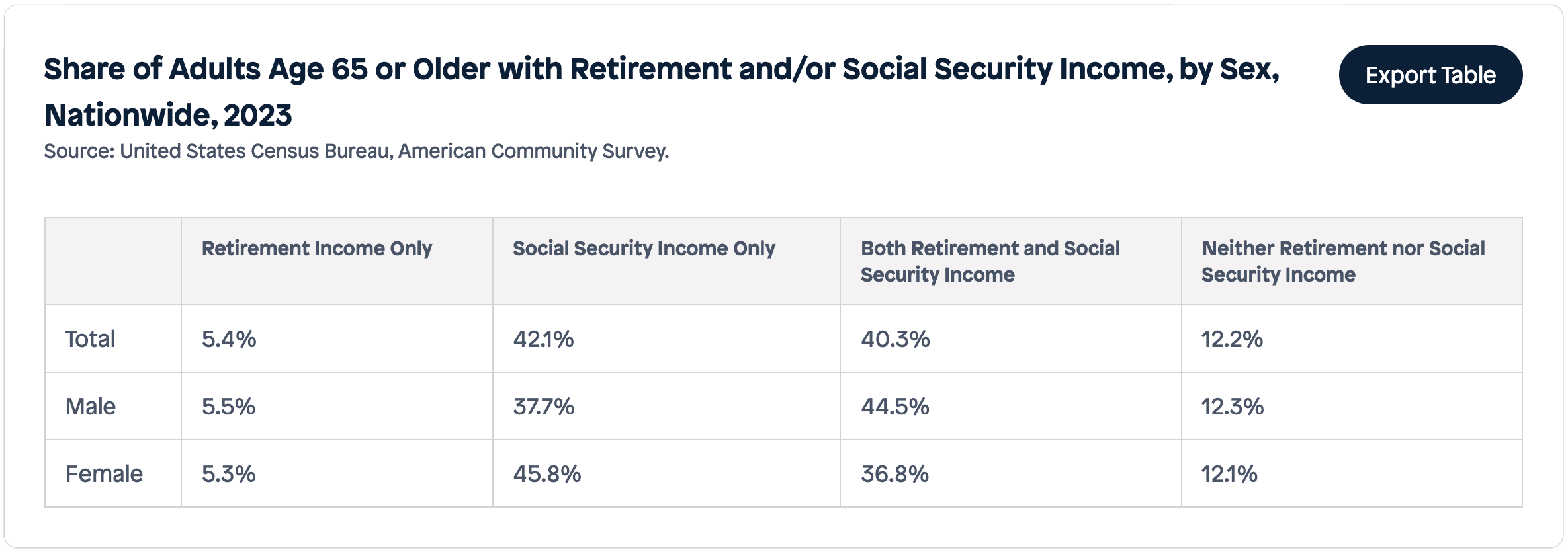

Lower lifetime earnings. Women are more likely than men to work in lower-paid sectors or in part-time roles that offer limited retirement benefits. They are also more likely to step away from paid work to provide caregiving and have fewer opportunities for advancement, which can reduce lifetime earnings and savings. A 2025 Transamerica Institute study found that women workers saved a median $3,000 in emergency funds, compared to $10,000 for men. Women age 65 and older (46%) are also more reliant on Social Security as their retirement income than men (38%). As a result, more than half of women age 65 or older who live alone are economically insecure.

Longer lifespans. Because women live longer than men on average, they often need their savings and income to last for more years, with 47% were worried about having enough money to live comfortably in retirement. Women’s greatest retirement fear is outliving their savings, and two-thirds of women ages 50 to 64 do not feel confident their savings will last through retirement. As a result, many women plan or expect to work after the traditional retirement age, either by necessity or preference. The U.S. Bureau of Labor Statistics projects that the number of people age 75 and older in the labor force will nearly double by 2030. For some, this “unretirement” reflects vitality and purpose; for many others, it reflects financial uncertainty.

Delayed or skipped health care. When asked if there was a time they or a member of their household did not seek care due to cost in the last three months, 26% of women ages 50 to 64 responded yes. Women ages 50 to 64 are more likely than older women and men to delay or forgo needed health care and medications, with 38% citing cost as a driver. Over time, these delays can worsen health conditions and increase financial strain. Transamerica Institute reports that women are concerned about the prospect of losing their independence or being unable to afford long-term care. For the nearly 25% of women ages 50 to 64 who are uninsured, the challenge is even greater, limiting access to health-related resources.

Increased caregiving responsibilities. About 43% of women have served as caregivers, and more than 85% have adjusted their work lives as a result, either by reducing hours or leaving the workforce altogether. Caregiving can play a significant factor in future finances, such as lower lifetime earnings, reduced retirement contributions, and fewer Social Security credits. Women are also more likely to continue caregiving into older age, whether supporting spouses, adult children, or grandchildren. The U.S. Department of Labor reports that 1.3 million women are the primary caregiver to grandchildren.

Opportunities to Strengthen Women’s Financial Security

The years leading up to retirement offer a variety of opportunities for policymakers and other interested stakeholders to improve women’s financial security. Cross-sector approaches are particularly promising, since women’s retirement readiness is shaped by challenges that no single sector can solve on its own. Examples of strategies include:

Women ages 50 to 64 face a set of interconnected challenges, but those same connections create opportunities for action. With intentional cross-sector policies, more coordinated systems, and targeted supports, states and communities can help build stronger financial security for women later in life.