FAQ - Employer-Based Health Plans

Can Employers Help Lower Health Care Prices through Self-Insured Plans? 10 FAQs about Employer-based Health Plans

December 1, 2023More than 150 million people—close to half of all Americans—get health insurance coverage through work, either through their own employer or as a dependent. Per person, health care spending in this population rose over 20% between 2017 and 2021, driven by increasing prices for health care services. Recent HCCI data show that price growth accounted for over 50% of the change in health care spending from 2017 to 2021. In contrast, growth in the volume of services accounted for 22% of the change in spending, and inflation accounted for only 7% of the change in spending. Employer-based insurance typically pays about twice as much as Medicare for the same services at the same hospitals, and pays about 20% more than Medicare for the average physician service with significant variation across the country.

Rising health care spending is a big problem for employers and employees. Over the past 10 years, the average premium for family coverage has grown by more than 50%, reaching almost $24,000 in 2023. Worker contributions to premiums have grown faster than wages (and inflation) since at least 1999.

TOP 10 FAQs

In addition to rising costs paid through premiums, Americans are paying more in cost-sharing for services and deductibles when they seek care. Recent survey data suggest that that over 40% of individuals and households do not have the necessary liquid assets to cover the typical deductible in an employer-sponsored health plan. As employers pay more for health care, this might lead to lower wages and/or less generous coverage, including higher employee premium contributions.

Below we answer 10 basic questions about the role of employers in lowering health care spending.

1. What role do employers play in U.S. health care spending?

As noted above, more than 150 million Americans get health insurance through an employer. Because so many people have employer-sponsored health insurance and employers make key decisions about the design of their employees’ health insurance, including negotiating how much they pay for the health care services their employees receive, employers have an opportunity to influence health care prices and spending.

Typically, both the employer and employee contribute to the cost of coverage, but the employer determines which health insurance to offer and how. For example, employers decide things like which insurance company to contract with and which benefits to cover. Employers also decide whether to purchase a health plan from an insurance company (fully-insured) or to collect premiums and pay directly for the cost of medical care (self-insured).

Health insurance is just one dimension of a company’s overall costs. Therefore, the money employers spend on health insurance affects their business decisions, including choices about employee wages and other benefits, such as retirement and leave policies. There is evidence that, as health care costs go up and employers pay more for health insurance, wages go down.

2. How do employers pay for their employees’ health insurance?

In general, there are two main types of plans that employers use to offer health insurance:

For example, when an employee goes to see the doctor, an insurance company would be responsible for reimbursing that visit in a fully-insured plan. In contrast, under a self-insured plan, the employer would be responsible for paying for the visit. (Note that In both cases, regulations apply to protect the privacy of individual employees´ health information.) Employers may use self-insured plans only, fully-insured plans only, or a combination.

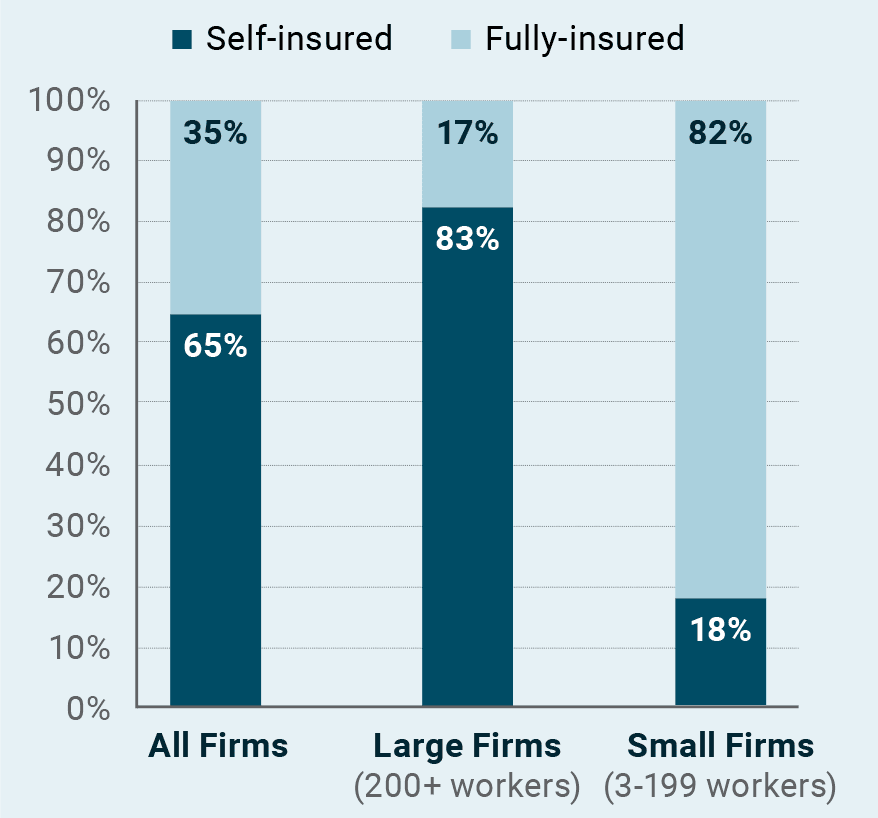

3. How many people are in self- insured plans?

About 99 million people, or two-thirds of those who get health insurance through an employer, are in a self- insured plan. This share has grown over time.

Employees who work in larger firms are much more likely to be in a self-insured plan. About 83% of employees with employer-sponsored insurance in large firms (200+) are in a self-insured plan compared to about 18% of workers in small firms.

Share of Employees in Self- and Fully-Insured Plans

Source: KFF. 2023. Employer Health Benefits 2023 Annual Survey.

Washington, DC.

4. Why do many employers decide to use self-insured plans?

Businesses could decide to use self-insured plans for several reasons. For instance, they may want more direct control over plan design, payment rates, and provider networks, which they can achieve more easily by offering self-insured plans than choosing from available fully-insured plans. They may also expect to save money by collecting premiums and paying directly for health services, which would allow them to keep any difference between what is collected and what is paid out.

In contrast, with fully-insured plans, the insurance company would keep any savings. (Note that for both self- and fully-insured plans, there are limits on how much insurers, whether employers or health insurance companies, can keep in terms of savings; regulations require that at least 80% of premiums collected for small firms and 85% for large firms are spent out on medical services.) Additionally, there is evidence that businesses, especially small ones, may choose to self-insure to avoid state regulations such as mandates to cover certain benefits (e.g., mental health, contraceptives) or providers (e.g., optometrists).

Frequently, self-insured employers rely on other companies to help them administer health insurance coverage. They work with benefits consultants, brokers, pharmacy benefit managers (PBMs), and third- party administrators (TPAs) to take on many of the responsibilities listed above, which creates a complex system of intermediaries involved in the administration of employer-sponsored insurance.

5. What is a third-party administrator (TPA) and what do they have to do with health care prices?

To help manage the administrative tasks of providing insurance coverage to employees, self-insured employers usually contract with outside companies, called third-party administrators (TPAs). These companies can help with many of the responsibilities self-insured employers take on, including:

TPAs help manage and administer health benefits for their clients—self-insured employer plans—but TPAs are not responsible for covering the cost of the health care services used by their client’s employees. Ultimately, the employers are responsible, and collect premiums from employees to offset the costs of those services. In this arrangement, therefore, employers that offer self-insured health plans should theoretically have strong financial incentives to bring down spending.

TPAs play a pivotal role in supporting employers’ plan administration, including enrollment and customer service, claim adjudication, reporting, and reimbursement, but TPAs are not typically financially responsible for an employer’s health care costs. In light of that, there are concerns that intermediaries do not have the same incentive as the employer to keep costs down while maintaining necessary coverage and quality, which contributes to rising spending in employer-sponsored health insurance.

6. (How) are self-insured plans regulated?

Most employee benefit plans, including self-insured health plans, are regulated under the framework of the Employee Retirement Income Security Act of 1974 (ERISA). ERISA lays out the basic standards employer benefit plans must meet; however, employers have substantial discretion in how the actual costs (e.g., employee contributions) and benefits are designed.

Further, self-insured plans are exempt from state regulations, including consumer protections that states might introduce and contributions to all-payer claims databases. Therefore, state initiatives related to insurance to lower costs or improve quality do not apply to self-insured plans. Changes to self-insured plans (e.g., coverage parity for mental health services, protections from surprise bills) typically require federal policymaking.

7. What factors work against employers’ ability to lower health care costs?

Since self-insured employers are financially responsible for their enrollees’ health care costs, they are at risk for rising spending. Accordingly, they have a strong incentive to manage the costs of their employees’ health care services. As noted above, prices are the primary driver of costs and should be an area of focus for employers who want to rein in high and growing health care spending. Employers’ ability to negotiate lower prices with hospitals and physicians who provide services to their enrollees, however, is limited for several reasons.

8. Are self-insured plans able to obtain lower prices on health care than fully-insured plans?

Not really. Recent HCCI research published in Health Affairs suggests that employers lack the leverage, resources, and information needed to negotiate lower prices for health care services that they are effectively purchasing. Among 19 common health care services, prices were higher in self-insured than fully-insured plans in most cases. For example, for endoscopies and colonoscopies, self-funded plans averaged about 8% and 6% higher prices, respectively, compared to fully-insured plans.

These findings are somewhat counterintuitive. That is, one may assume that self-insured employers could obtain better prices than fully-insured employers for a couple of reasons: First, employers with self-insured plans are typically larger and therefore would have better negotiating power. Second, employers with self- insured plans have greater financial incentive to negotiate lower prices on health care services because they would save their company money more directly. However, these results suggest that employers are not able to negotiate lower prices on behalf of their employees, likely related to the factors described above (e.g., provider consolidation, reliance on intermediaries, and a lack of price information).

Additionally, other factors affecting the cost of employer-based coverage may play a role, but are not evident in this pricing analysis. For example, self-insured employers may have different arrangements on employee cost sharing and provider networks.

For common services, self-insured employer plans are paying higher prices than fully-insured plans

Source: Sen, Chang, Hargraves. (2023.) Health Care Service Price Comparison Suggests That Employers Lack Leverage To Negotiate Lower Prices. Health Affairs, 42(9): 1189-1312

9. Do employers have any tools to lower prices in self-insured plans?

Employers can take a more active role in demanding and seeking out information and data on health care prices and use; these data are the absolute minimum necessary to conduct any sort of price negotiations. To increase leverage, employers are beginning to join forces in coalitions to negotiate prices, such as Colorado’s Peak Alliance. Where feasible, employers may also consider doing more health care data analytics and plan-related decision-making (e.g., payment policies) on their own rather than relying on intermediaries to get the best value.

10. How can policymakers support employers in lowering prices in self- insured plans?

Given limitations on employers’ ability to negotiate, successfully reducing prices in commercial health insurance markets will require state and federal policy intervention. Even though self-insured health plans are exempt from state regulations, state policymakers could consider the following tools to lower prices in self-insured plans: regulating providers (e.g., through price caps on high-priced providers) and pharmacy benefit managers, investing in price transparency, and taking steps such as increased monitoring of consolidation to prevent or mitigate anticompetitive behaviors among health care providers.

As noted above, federal policy is needed to lower health care prices among self-insured plans, including regulating self-insured plans directly as Congress did when it introduced protections against surprise bills in the No Surprises Act and coverage parity requirements for mental health services, which apply to all health plans. Official antitrust enforcement activities are also critical to preventing price-rising consolidation. Finally, while not directly affecting prices, federal policymakers could advance important initiatives to make self-insured health plan data available, including through increased price transparency requirements, all-payer claims databases, and facilitating employer access to the claims data of their own self-insured employees. These efforts have the potential to facilitate employer price negotiations, but must be structured in a way that makes these data actionable for employers.

ABOUT HCCI

The Health Care Cost Institute is an independent, non-profit research institute. HCCI’s mission is to get to the heart of the key issues impacting the U.S. health care system by using the best data to get the best answers. HCCI stands for truth and consensus around the most important trends in health care, particularly those economic issues that are critical to a sustainable, highperforming health system. Our values are simple: health care claims data should be accessible to all those who have important questions to ask of it. Health care information should be transparent and easy to understand. All stakeholders in the health care system can drive improvements in quality and value with robust analytics.

Learn more at healthcostinstitute.org

Follow @HealthCostInst

ABOUT WEST HEALTH

Solely funded by philanthropists Gary and Mary West, West Health is a family of nonprofit and nonpartisan organizations, including the Gary and Mary West Foundation and Gary and Mary West Health Institute in San Diego and the Gary and Mary West Health Policy Center in Washington, D.C. West Health is dedicated to lowering healthcare costs to enable seniors to successfully age in place with access to high-quality, affordable health and support services that preserve and protect their dignity, quality of life and independence.

Downloads

HCCI-10-FAQs-December-2023.pdf

Download